Three-Domain Secure (3DS or 3-D Secure) is a XML-based messaging protocol to enable cardholders to authenticate themselves with their card issuer while making card-not-present (CNP) online purchases. 3-D Secure helps to prevent unauthorised CNP transactions and protects the merchants and issuers and cardholders from fraud on cards.

3-D Secure facilitates the exchange of cardholder data between CNP transaction participants – cardholder, merchant, card issuer and payment system. 3-D Secure version 1.0 was initially developed by Visa and marketed as Verified by Visa (VbV) since early 2000s. Services based on the 3-D Secure 1.0 have also been adopted by MasterCard as MasterCard SecureCode (MCC), by JCB International as J/Secure and by American Express as American Express SafeKey.

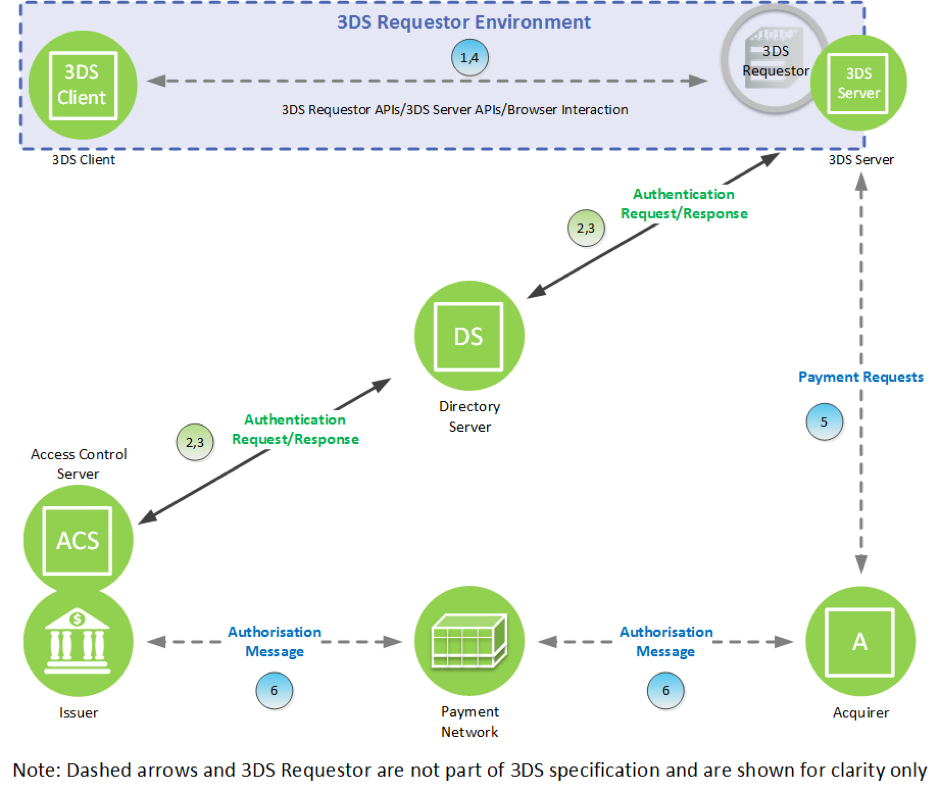

The three domains consist of the merchant / acquirer domain, issuer domain, and the interoperability domain (e.g. payment systems). This is simplified diagram of 3-D Secure 1.0 process workflow:

3-D Secure 1.0 Diagram

The main benefit of 3-D Secure is shifting the possible fraud responsibility from the merchant to the card issuer, which reduces chargebacks. Nevertheless, many merchants don’t use the 3-D Secure, due to that the benefit form the less chargeback does not compensate losses in conversion rates and costs of service.

Main disadvantages of version 3D-Secure 1.0 are:

Due to above mentioned drawbacks and for better reflecting current and future market requirements, the payments industry recognised the need to create a new 3-D Secure specification. Thus since January 2015, EMVCo, a company which is collectively owned by American Express, Discover, JCB, MasterCard, UnionPay and Visa, were developing the EMV 3DS 2.0 Specification and in October 2016, the specs for 3-D Secure 2.0 was published.

EMVCo declares that new specification of 3-D Secure 2.0:

As 3-D Secure 2.0 has to support new authentication flows, it extends the 3-D Secure ecosystem by introducing new components and defining new terms. All components present in Acquirer (Merchant) domain now named by collective term “3DS Requestor Environment”.

The 3DS Server - system that handles online transactions and facilitates communication between the 3DS Requestor and the DS, replaces term Merchant Server Plug-in (MPI).

3DS Client - the consumer-facing component allowing cardholder interaction with the 3DS Requestor. For example – online-shopping web application or online-shopping mobile application. This can be implemented via in-app (3DS SDK) and browser based purchases (3DS Method). Both could be integrated with the 3DS Requestor for a smooth online shopping experience.

3DS Requestor - the initiator of the 3-D Secure 2.0 authentication request (AReq). For example, this may be a merchant or a digital wallet requesting authentication within a purchase flow.

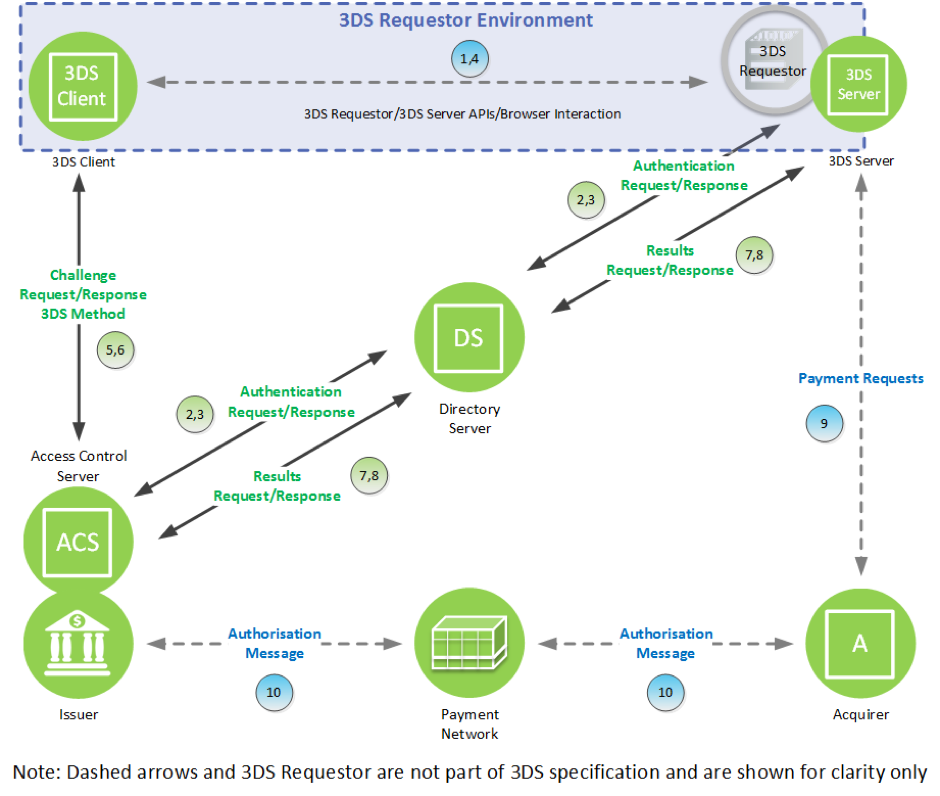

The biggest difference since 3DS 1.0 is the Frictionless flow which allows issuer to approve a transaction without cardholder interaction based on risk-based-authentication performed in the ACS. (Steps 1-4 at the figure below)

Challenge flow has got changed way of communication from the Issuer to Merchant. In 3DS 2.0 the result of challenge is communicated through the DS. (Step 6 at the figure below) Thus, Merchant is informed about the authentication results via a separate channel, which is more secure.

Non-payment Authentication - 3-D Secure 2.0 also introduces special non-payment customer authentication, which can be used for cardholder Identification & Verification (ID&V) for mobile wallets and the secure request of tokens for card on file. This flow is similar to the 3-D Secure 2.0 authentication flow during a purchase on the web shop, but it does not include payment specific steps like payment initiation, confirmation etc.

Comparing 3DS 1.0 version 2.0 introduces new messages and change the names for the messages that are exchanged between the components. A new message type is the Result message (RReq and RRes), which is exchanged between the Issuer (ACS) and the Merchant (3DS Server) to communicates the result after cardholder verification.

New data fields were added to messages to support new functionalities. Also, 3-D Secure 2.0 defines messages with JSON, compared to XML in version 1.0.

This table illustrates changes in messages:

| 3DS Transaction Phase | 3DS 1.0 | 3DS 2.x |

| Ranges cache loading | CRReq/CRRes | PReq/Pres (Preparation Message) |

| Participation/enrollment check | VEReq/VERes | AReq/ARes (Authentication Message) |

| Frictionless authentication | N/A | Part of AReq/ARes |

| Challenge authentication and confirmation |

PAReq/PARes | CReq/CRes (Challenge Message) + RReq/RRes (Results confirmation Message) |

3-D Secure 2.0 makes deprecated the following authentication methods, which are not considered to be secure:

They are not allowed for Primary or Fall-back Authentication.

Risk-based Authentication (RBA) becomes a highly recommended to be used.

Usage of RBA is the mechanism, which allows Issuer to implement frictionless payments for low risk transactions. That requires issuer to have risk engine implemented and appropriately configured set of risk rules created. Issuers may implement own RBA algorithm or use independent vendors for such risk engine implementation – like Fraud Scoring Server (FSS) from Modirum.

Using of biometric authentication devices and flows become also a highly recommended by payment systems. This technology is becoming mature enough to provide good security and performance level, as well as positive consumer experience at checkout. Available methods are fingerprint match, voice and facial recognition.

Support of Mobile devices is mandatory with 3-D Secure 2.0. Any used authentication flow should grant support for mobile devices. That means all authentication flows, which do not provide it will not be granted with 3-D Secure 2.0 certification by EMVCo nor by payment systems.

The Out-Of-Band authentication means usage of two different channels or two factors in verification process. Both of them should be applicable for in 3-D Secure 2.0. For example, primary authentication may be passed by voice or facial recognition, while secondary pass may be granted with SMS OTP.

The only browser redirection can be used with 3-D Secure 2.0. Obsolete native (application) redirection should be replaced by other appropriate authentication method. Browser redirection authentication according 3-D Secure 2.0 has to support mobile devices and be able to work in iFrame.

In Background authentication method ACS is working as a proxy server. It forwards both PAReq and VEReq messages to the issuer’s background server instead of processing them. This approach is fine from 3-D Secure 2.0 perspective if issuer implements a proper authentication method.

EMVCo published the EMV® 3-D Secure – Protocol and Core Functions Specification version 2.0 in October 2016 and EMV® 3-D Secure – SDK Specification in January 2017.

Currently drafts of the next versions of the documents are being discussed.

At Q3-Q4 2017 EMV® 3-D Secure 2.0 certification for software and service vendors should become available.

Payment systems defines their own certification requirements for 3-D Secure 2.0. MasterCard already updated their MasterCard Identity Check program for 3-D Secure 2.0. Visa should publish their requirement in closest time.

Since EMVCo certification details are yet unavailable, it is still expected that 3-D Secure 2.0 needs to be implemented during 2018. 3-D Secure 1.0 will not be supported as of 1.1.2020.